Shipping Slowdown Exposes Vulnerability of US Economic Growth

[Stay on top of transportation news: Get TTNews in your inbox.]

Real economic activity in the U.S. is slowing sharply. This is showing up in lower demand for new trucks and autos, and a tailing off in freight volumes, leaving transport stocks facing more downside.

Heavy truck sales in the U.S. are a very good leading indicator of economic activity, with 65% of the dollar value of North American freight moved by trucks. But new truck sales have been falling sharply and are now down 23% on an annual basis. New auto sales are falling at a similar rate. Truck and auto sales combined are falling at a rate previously only associated with recessions.

This is not a recession prediction. Recessions are signaled by a rapid regime shift across many areas of the economy and markets, and there is no sign the U.S. is in the process of this happening. Nonetheless, this sharp decline in vehicle sales shows slowing growth is in the mail.

Freight volume growth has also been slowing. Annual growth in containers loaded at the Port of Los Angeles is steadily heading down to 0% after hitting 20% last year. Lockdowns in China are clearly having an impact in the U.S. Cities and regions accounting for over 40% of China’s 2020 GDP are in full or partial lockdown. The Shanghai freight index is 13% lower than it was six weeks ago, the sharpest decline seen in the 10-year history of the index.

Shipping rates have been falling, but this is academic as it is virtually impossible — while such a draconian lockdown is in place — for exporters to load boxes in their warehouse and move the goods onto the ships.

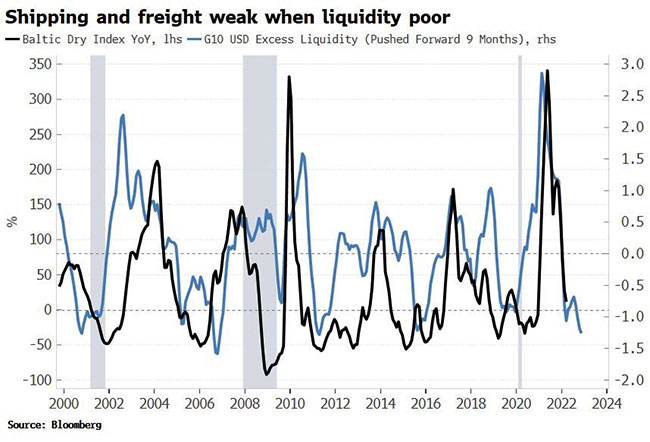

Lockdowns in China may be a proximate cause of falling shipping rates, but the remote cause is the fall in global liquidity as central banks step back from historically loose monetary policies to try to stem inflation. Global liquidity has collapsed and points to continued depressed shipping rates in the coming months.

That commodities, their movement around the world, and liquidity are intrinsically linked has become starkly clear in this cycle. As a commodity producer, if you don’t have the liquidity to cover the margin on your short futures positions, bankruptcy means you can’t ship and deliver your commodities, exacerbating the rise in prices and triggering more margin calls.

This liquidity and economic-demand driven decline in shipping and truck usage points to underperformance of transport stocks. The S&P transport index is down 11% from its high of last month. Transports and autos are roughly flat to the S&P year-to-date, so should begin to lag. Furthermore, being underweight medium- to high-duration sectors is a good idea when in an inflationary regime.

Want more news? Listen to today's daily briefing below or go here for more info: